18f-4 Regulatory Reporting Made Easy Through Automation

A Summary of the new SEC regulation, Rule 18f-4, and how funds can fulfill the reporting requirements through automation.

1) What is the 18f-4 Regulation?

In a couple months registered funds will be required to comply with Rule 18f-4, an SEC regulation which requires risk monitoring for ‘40 Act funds that make use of derivatives and certain related transactions. The new regulation is onerous as it requires daily exposure and VaR monitoring as well as backtests and stress tests.

In essence, the rule requires registered funds with more than 10% exposure in derivatives such as options, futures and short positions to comply with VaR rules as follows:

A. Relative VaR: The VaR of the fund should be smaller than 2x the VaR of a designated reference portfolio (DRP). The DRP can be an index, another fund or the fund itself, without the derivatives (the securities portfolio).

B. Absolute VaR: The VaR of the fund should be smaller than 20% of the fund’s net assets.

The Rule does not require a specific approach to calculate VaR (parametric, historical or monte carlo), and only specifies that the model should capture various risk factors, use 3 years of historical data and use a 99% confidence level.

Furthermore, 18f-4 requires stress tests to be performed and historical VaR exceedances to be recorded.

2) Everysk Automations

Everysk is a technology company specialized in automations for the financial sector. Our platform allows professionals without any coding experience to orchestrate sophisticated daily workflows. Our workflows are tailored to portfolio management, regulatory/compliance reporting, pre-trade compliance, risk and liquidity monitoring, anti-money laundering and many other financial applications.

Building a workflow is easy: All you need to do is drag and drop robots from the library to the design canvas

Our robots are designed for financial applications and they perform tasks, such as:

Explode the content of an invested fund into another root fund

Insert intra-day trades into appropriate books from start-of-day (SOD) portfolios

Aggregate positions coming from different brokers into a holistic portfolio

Call our multi-asset, forward-looking calculation engine to perform risk and liquidity analysis

Generate datalakes containing a blend of Everysk calculations and clients’

Perform complex data explorations and set dynamic criteria

Connect with outside APIs, distribute reports and alerts using email, Teams or Slack

Perform conditional tests, branching the logic of the workflows

And many other tasks

Our workflows are designed to benefit from highly scalable infrastructure in the cloud. Report templates can be easily designed and can dynamically bind elements from the automation for scalable report generation and distribution.

3) An Automated Solution to 18f-4 Reporting

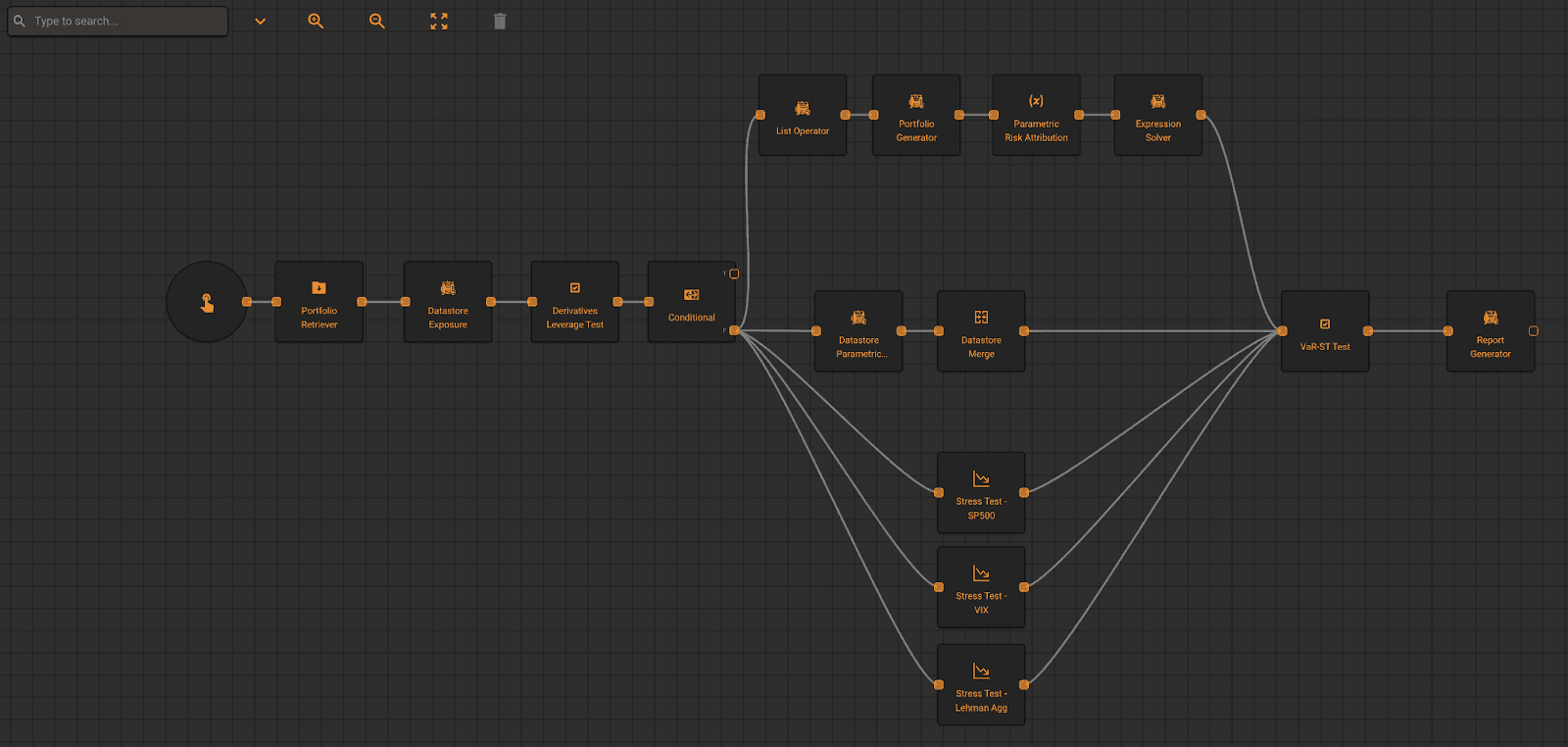

Everysk has built a workflow specially designed for 18f-4. Clients can plug and play a workflow that would automatically comply with all 18f-4 requirements on a daily basis. This is what our out-of-the-box 18f-4 workflow looks like:

It automatically tests if you have more than 10% exposure in derivatives. If you have more than 10%, it automatically calculates portfolio VaR and checks the relative and absolute VaR limits for you. Everysk has access to market data and our own risk engine so all that’s required is the portfolio holdings. Everysk is also capable of setting up email alerts if there is a VaR exceedance or breach of any of the tests.

The workflow generates stress tests and also backtests PL with VaR forecasts. The whole process is digitized, saving hours of daily work. All the daily tests are securely stored in your account and readily auditable.

A sample report can be found in the link:

Please contact us at contact@everysk.com to learn more about our automations and the 18f-4 module.